Access the capital you need to fulfil large orders, optimise cash flow, and grow your retail or DTC business without delays. Triffin’s supply chain financing lets brands secure inventory, get paid faster, and maintain predictable working capital, so your business can scale efficiently while keeping suppliers and operations fully supported.

• Get funding quickly when needed

• Protect cash flow & avoid operational bottlenecks

• Fund inventory before revenue arrives

Triffin combines fast, flexible purchase order financing with an AI-powered financial ops platform, designed to help consumer brands manage cash flow, reduce operational stress, and scale efficiently.

Our platform streamlines funding, automates time-consuming finance tasks, and provides actionable insights, giving you full visibility over your margins, costs, and performance.

With Triffin, brands can make confident growth decisions, fulfil larger orders, and grow without the burden of spreadsheets or manual processes.

Funding that adapts quickly to seasonal demand and growth cycles

Automated agents reduce manual work and keep financial operations running smoothly

Get cash from retail and wholesale orders immediately to protect cash flow

Supply Chain Financing (SCF) is a set of financial solutions and technologies designed to optimise cash flow and reduce costs for all parties involved in a supply chain transaction (typically a buyer, a supplier, and a financial institution). It allows businesses to better align their payment schedules with their actual revenue cycles.

At its core, SCF speeds up suppliers' payments while extending the buyer's payment terms, strengthening the entire supply chain's financial health.

Supply chain financing comes in several types, each designed to solve different cash flow challenges for buyers or suppliers:

A. Reverse factoring (supplier finance)

The buyer arranges for a financier to pay suppliers early.

Examples: A retailer agrees with a bank to pay its supplier immediately for goods, while the retailer extends its own payment terms by 60 days. The supplier gets cash faster, and the retailer keeps working capital longer.

B. Dynamic discounting

The buyer pays the supplier's invoice early in exchange for a discount.

Example: A DTC brand pays its packaging supplier two weeks early in return for a 2% discount on the invoice, saving money while helping the supplier with cash flow.

C. Factoring/receivables finance

The supplier sells its unpaid invoices to a financier at a discount.

Example: A beverage company sells its outstanding invoices to a finance provider and receives 90% of the invoice value immediately, instead of waiting 30–60 days for the customer to pay.

D. Inventory financing

A loan secured against inventory to purchase or hold stock.

Example: A cosmetics brand takes a loan against its finished stock to fund a new product launch, ensuring shelves are stocked without using existing cash reserves.

E. Purchase order (PO) financing

Funding to fulfil a specific confirmed customer order.

Example: A food brand receives a large wholesale order but lacks cash to buy raw ingredients. PO financing provides the funds to produce the order, which is repaid once the customer pays.

F. Other notable solutions:

• Payables Finance: A bank pays suppliers early based on the buyer’s credit.

• Letter of Credit (LC) Financing: Banks guarantee payment for international shipments, which suppliers can use for financing.

• Pre-Shipment & Post-Shipment Financing: Provides funds before or after goods are shipped to maintain production and cash flow.

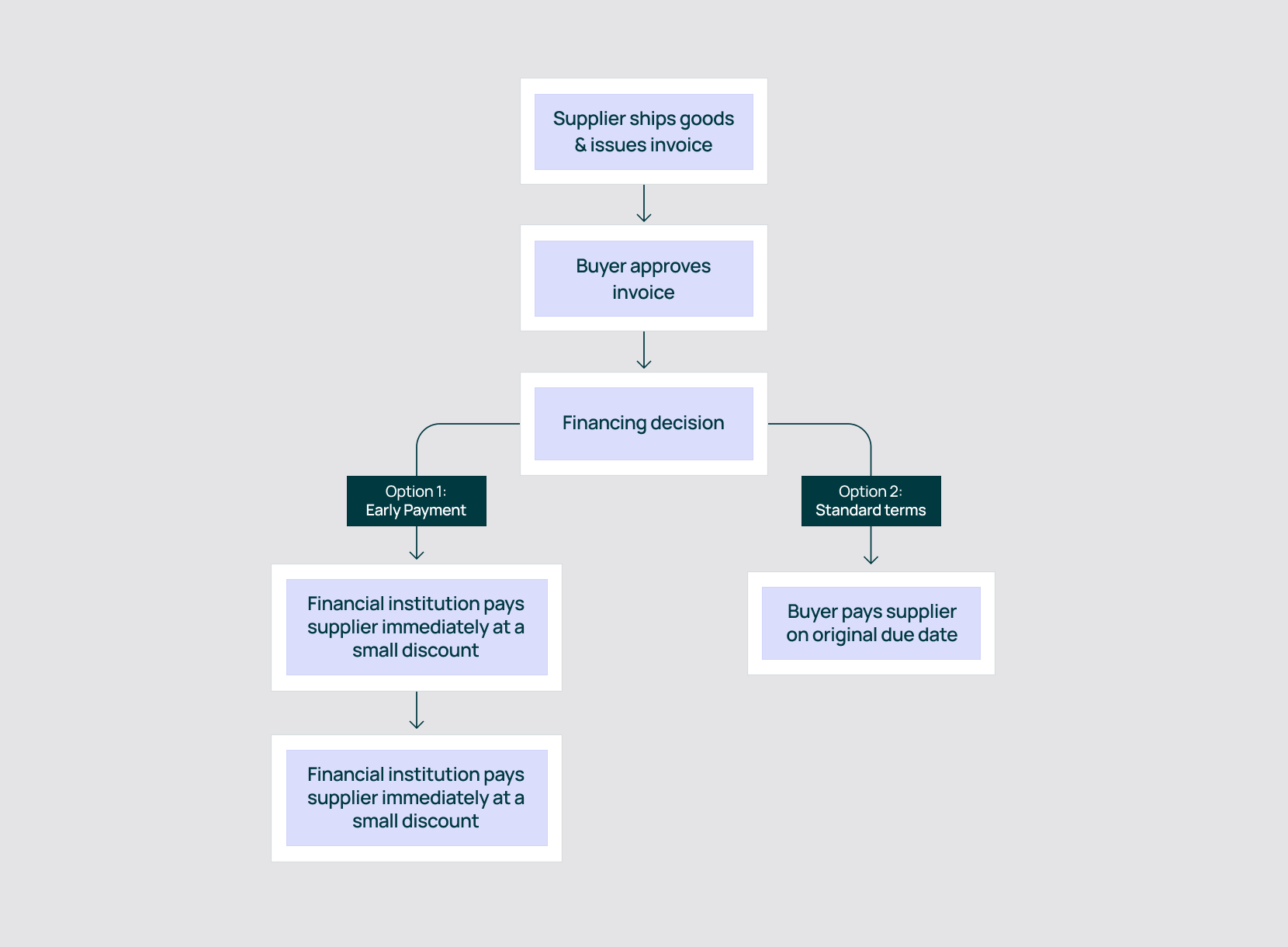

1. Transaction and invoice

The supplier delivers goods or services and issues an electronic invoice, usually with standard payment terms, such as net 60 days.

2. Invoice approval

The buyer reviews and approves the invoice, confirming the debt is valid and will be paid.

3. Upload to SCF platform

Traditional SCF platforms make approved invoices visible to suppliers, buyers, and financiers through a shared platform.

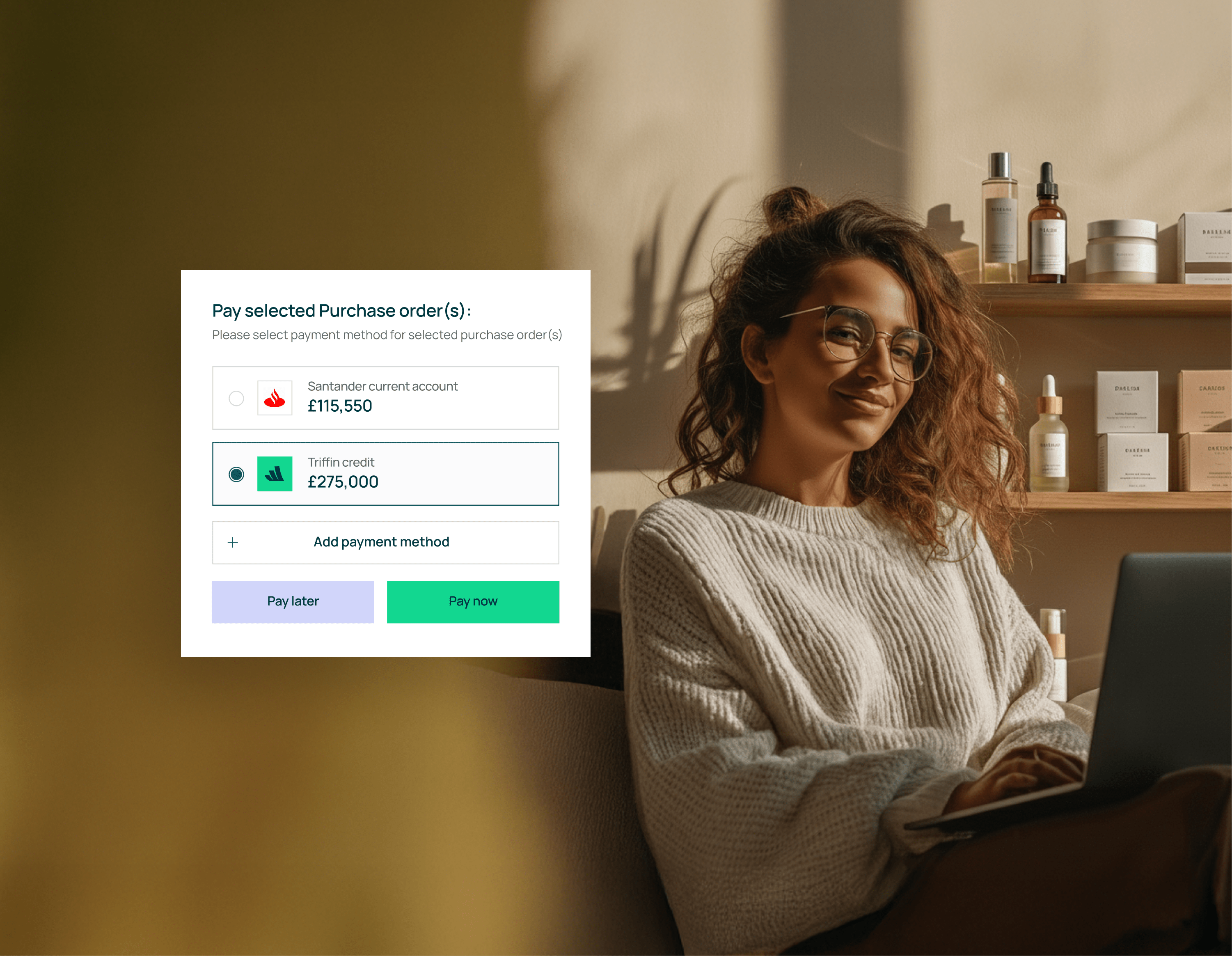

However, confidential financing solutions like Triffin Credit work differently. Your suppliers never know you're using financing, preserving your business relationships and negotiating position.

4. Supplier’s choice

In traditional supply chain finance programs, the supplier can request early payment for the invoice or wait for standard payment terms.

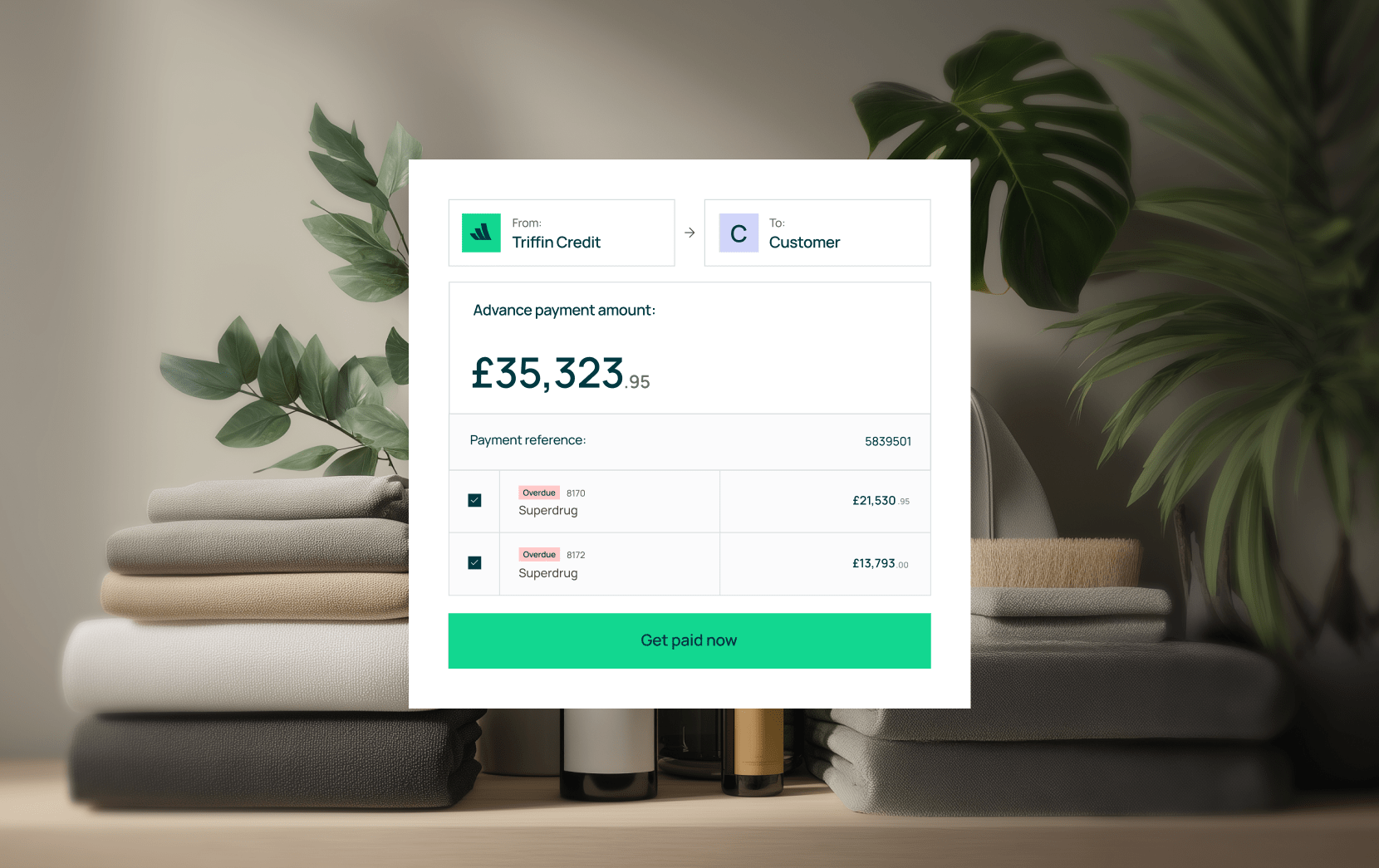

5. Early payment by financier

If the supplier chooses early payment, the financier pays the invoice amount minus a small pre-agreed financing fee, often within 24–48 hours.

With Triffin Credit, the process works differently. You draw funds from your revolving credit facility as needed, independent of supplier involvement. Your suppliers are paid according to your normal terms, while you access working capital immediately based on your brand's creditworthiness. No supplier notification, no supplier approval required.

6. Settlement on due date

On the invoice’s original due date, the buyer pays the full invoice amount to the financier.

Note: A newer variant, called post-maturity financing, works slightly differently. Here, the supplier is paid on the original due date by a payment service provider, which then creates an extended payable with the buyer (e.g., 30–60 days). This can help maintain the accounting treatment as a trade payable rather than debt, though it is subject to scrutiny.

Optimises working capital

For buyers, SCF allows payment terms to be extended, meaning they can hold onto cash longer and manage liquidity more effectively. Suppliers benefit by converting approved invoices into immediate cash, improving their day-to-day cash flow and reducing gaps between paying expenses and receiving revenue. This ensures smoother operations and the ability to fulfil orders without delay.

Lowers financing costs

Suppliers gain access to capital at rates linked to the buyer’s stronger credit profile, often cheaper than traditional standalone loans. Buyers also benefit from cost-neutral programmes or the opportunity to negotiate early payment discounts. This creates a more efficient financing structure across the supply chain, reducing the overall cost of capital for all parties.

Strengthens supply chain relationships

SCF improves partnerships by offering suppliers faster payment options without harming buyer cash flow. Suppliers gain financial stability and predictability, which builds trust and secures ongoing revenue relationships. Over time, this strengthens long-term collaboration, reduces supplier turnover, and enhances reliability across the supply chain.

Enhances supply chain resilience

By improving supplier liquidity, SCF reduces the risk of financial distress, helping suppliers withstand market fluctuations and continue delivering products on time. Buyers benefit from a more stable supply chain, with fewer disruptions affecting production, inventory, or customer fulfilment.

Improves operational efficiency

Digital SCF platforms automate the procure-to-pay cycle, making invoice approvals, payments, and reporting faster and simpler. Suppliers face less administrative burden, and buyers can streamline payables management, freeing teams to focus on strategic growth rather than manual financial tasks.

Increases financing efficiency and access

SCF enables SMEs to unlock capital based on transaction data, alleviating funding constraints. Buyers can manage payables efficiently, optimising working capital across multiple suppliers while ensuring suppliers are supported.

Supports broader business performance

Beyond cash flow, SCF can align with corporate financial and ESG goals. Suppliers can invest in growth, innovation, and sustainability initiatives, which strengthens overall corporate performance and enhances reputation.

Accounting opacity and financial health misrepresentation

One major criticism of SCF is that large corporate buyers can classify financing as a trade payable rather than debt. This can artificially enhance the buyer’s financial health, masking true leverage and debt levels. Investors, auditors, and lenders may be misled, and high-profile corporate collapses, such as Carillion, have been linked to undisclosed SCF obligations.

Risk of sudden program withdrawal for suppliers

SCF programmes depend on the relationship between the buyer and financier. If the buyer’s creditworthiness deteriorates or the financier changes policies, suppliers can lose access to early payment with little notice, creating a sudden cash flow shock.

Supplier lack of control and extended terms

Suppliers often surrender control over invoice approval and payment timing to the buyer and financier. Programmes can slow payments compared to alternative financing, and buyers may extend payment terms unilaterally, forcing suppliers to pay fees for early access to cash.

This drawback doesn’t apply to Triffin Credit, as we offer a flexible revolving credit facility which puts control back with you. You decide when to draw funds against your own credit line, independent of any single buyer’s payment terms or approval timelines.

Complex implementation and coordination

Launching an SCF programme requires cooperation between buyers, suppliers, and financial institutions. This adds administrative and technological complexity, with supplier onboarding onto digital platforms frequently cited as a major hurdle.

Supplier dependency and potential for margin erosion

While SCF can strengthen relationships, suppliers may become overly dependent on a single buyer’s programme. Fees for early payment, combined with any buyer-imposed discounts, can erode profit margins.

With Triffin Credit you can access 100% of an invoice's value, helping protect your margins instead of eroding them.

Concentration risk and systemic vulnerabilities

SCF concentrates financial risk on the credit of a single large buyer. If that buyer fails, the impact cascades through its supplier network, potentially causing widespread disruption across the supply chain.

Increased exposure to cybersecurity threats

SCF relies heavily on digital platforms for invoice processing and payment. This introduces vulnerabilities to cyberattacks, data breaches, and technical failures that could compromise sensitive information and disrupt financial operations.

Learn more about how Triffin can help your business

Once approved for Triffin Credit, you can access your revolving credit facility within 48 hours. This allows you to fund inventory purchases or request early payment on invoices quickly, helping maintain smooth operations and predictable cash flow.

Yes. Triffin connects seamlessly with platforms like Shopify and accounting software such as Xero. Our AI agents then automate cash flow forecasting, invoice chasing, and pay runs, creating a unified hub for managing your financial operations.

Absolutely. Triffin is designed for modern consumer brands. For DTC businesses, inventory financing helps prepay for stock to meet demand spikes, while AI tools automate manual finance tasks, from reconciling payouts to forecasting cash flow.

Unlike traditional factoring, Triffin Credit is a flexible, revolving facility. You draw funds as needed against your credit line, often at lower overall costs, without selling individual invoices at a high discount. Everything is managed transparently through your Triffin account.

Yes. Many brands start with our AI finance platform to automate cash flow forecasting, pay runs, and invoice collection. You can add Triffin Credit at any time to bridge working capital gaps and fund your growth.

Triffin Credit gives you flexibility in how and when you repay. Choose between monthly payments or a bullet repayment (paying principal plus fees in one lump sum at the end of the term). You can also select a repayment timeframe between 2–6 months to suit your cash flow cycle.

“Triffin gives me the insights and financial confidence - every single day down to a granular level, I can see my financials - It's my number one”

“Triffin is a game-changer for cash flow! I love how the sales & marketing agent splits our performance by market”

“With Triffin we can launch new markets and new product lines in a low-risk way, it’s been a fundamental change in how we run the business leading to triple-digit growth.”

“The financial analyst agent keeps our business on track. It’s ability to surface COGS/Postage/Pick & Pack on a per order level makes analysing our margins at a granular level so easy, without needing spreadsheets.”

“Getting agent reminders on what to pay and when removes a lot of the hard, manual admin work, it makes our weekly pay-runs easy. I love the analyst agent's 3D avatars!”