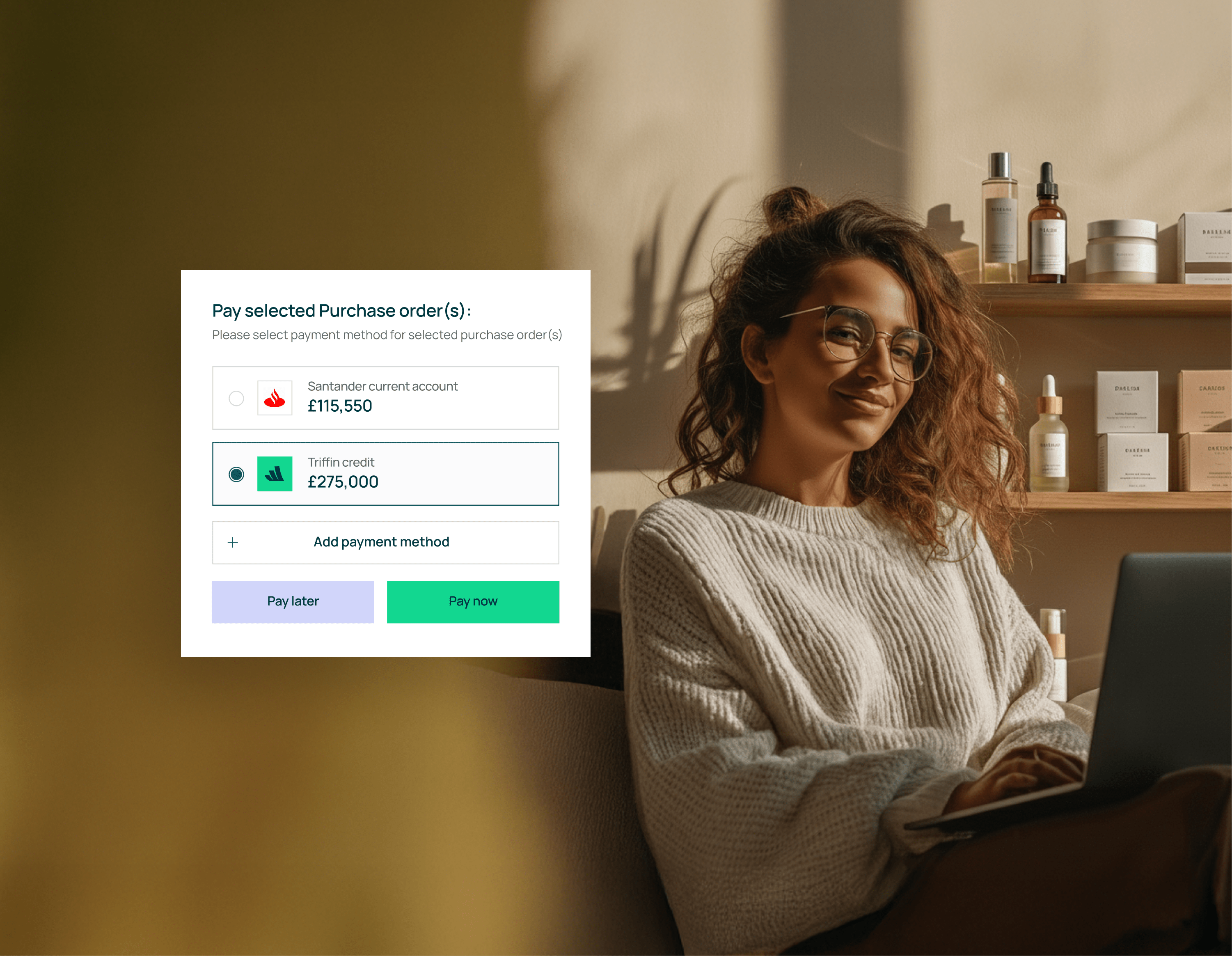

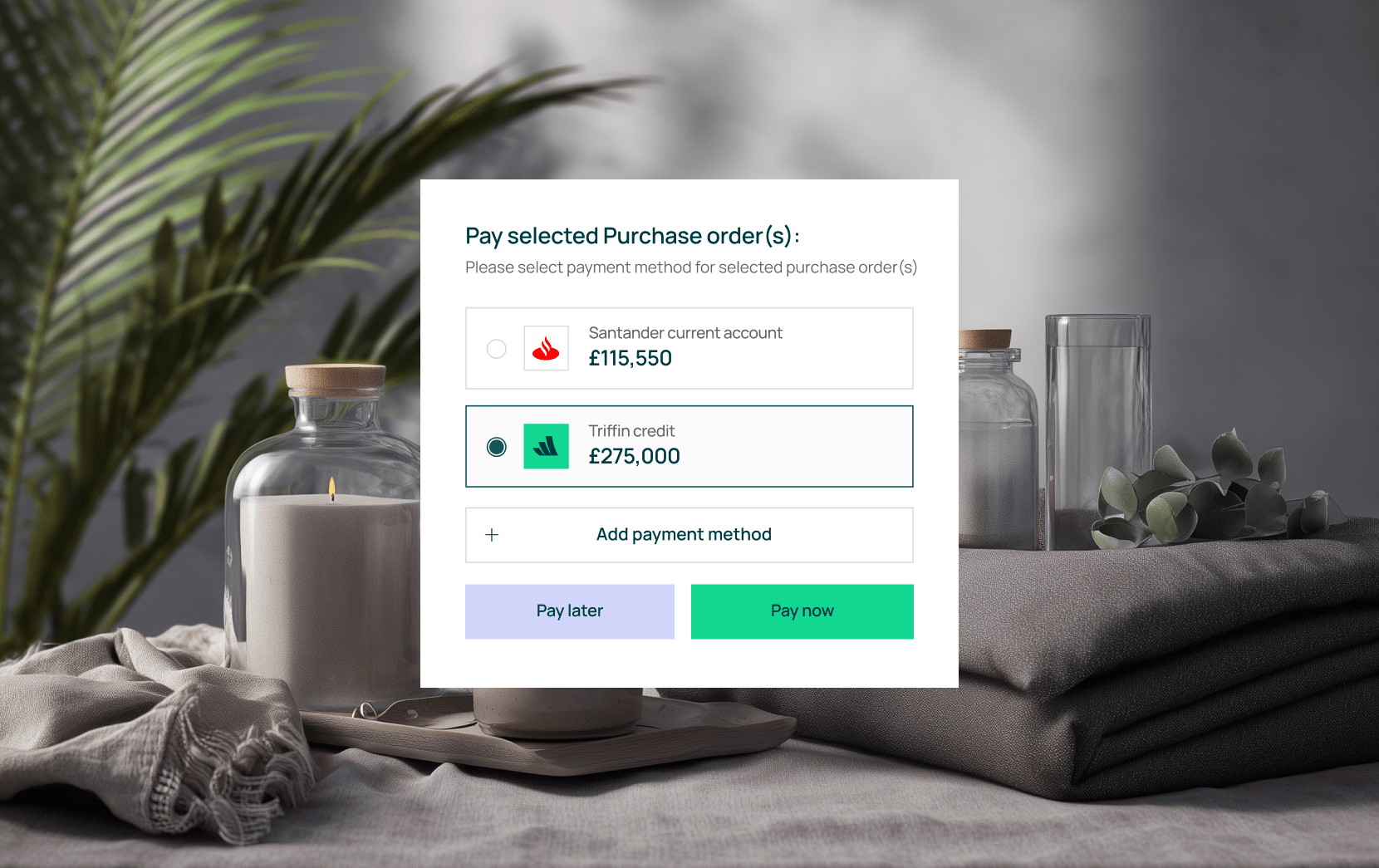

Unlock fast funding to secure inventory, fulfil large orders, and keep cash flow predictable. Triffin provides flexible purchase order financing designed for retail and ecommerce brands, helping you bridge cash gaps, reduce stress, and scale without slowing down. Apply in minutes and access the capital you need to grow with confidence.

• Accept larger orders from B2B customers with ease

• Protect cash flow & avoid operational bottlenecks

• Fund inventory before revenue arrives

Triffin combines fast, flexible purchase order financing with an AI-powered financial ops platform, designed to help consumer brands manage cash flow, reduce operational stress, and scale efficiently.Our platform streamlines funding, automates time-consuming finance tasks, and provides actionable insights, giving you full visibility over your margins, costs, and performance. With Triffin, brands can make confident growth decisions, fulfil larger orders, and grow without the burden of spreadsheets or manual processes.

Get capital quickly to fund inventory and large purchase orders

Revolving credit supports inventory, growth, and operational needs

Easily connect across all your retail and e-commerce channels

Purchase order financing is a funding solution that helps businesses pay suppliers upfront to fulfil large B2B customer orders. Instead of using your own cash or waiting to accumulate funds, a financing provider covers the cost of producing or sourcing the products your customer has ordered.

This type of financing is commonly used by consumer brands that sell via retail and wholesale channels (like supermarkets, department stores, and independent retailers) to meet demand without overextending cash reserves.

While providers typically offer a core PO financing product, its features can be adapted to suit different business situations and order requirements.

A. Single-order financing

Funding is provided for an individual customer order. Once your customer pays the financier, fees are deducted, and the remaining profit is sent to your business.

Example: A nutrition brand receives a £60,000 wholesale order from a UK retailer and uses PO financing to pay the supplier upfront, fulfiling the order on time.

B. Multiple orders/recurring financing

While not a formal “revolving credit line”, businesses can finance successive orders by working closely with the lender. Establishing a relationship can streamline approvals for recurring needs.

Example: A homeware distributor funds three consecutive monthly orders from different retailers, using the same financier to reduce paperwork and approval times.

C. Partial vs. full funding

Lenders may cover 80–100% of supplier costs, with the business covering the remainder if funding is partial. The percentage depends on your customer’s creditworthiness, supplier reliability, and your profit margins.

Example: A cosmetics company receives a £25,000 order but covers £5,000 of supplier costs themselves while the financier funds the remaining £20,000.

D. International orders

PO financing can support importing and fulfiling overseas orders. It covers supplier prepayments, longer shipping times, and additional costs such as import duties or currency differences, often using Letters of Credit to guarantee payments to foreign suppliers.

Example: A food and drink business importing ingredients from Europe uses PO financing to pay the supplier and ship products to fulfil a £50,000 international order.

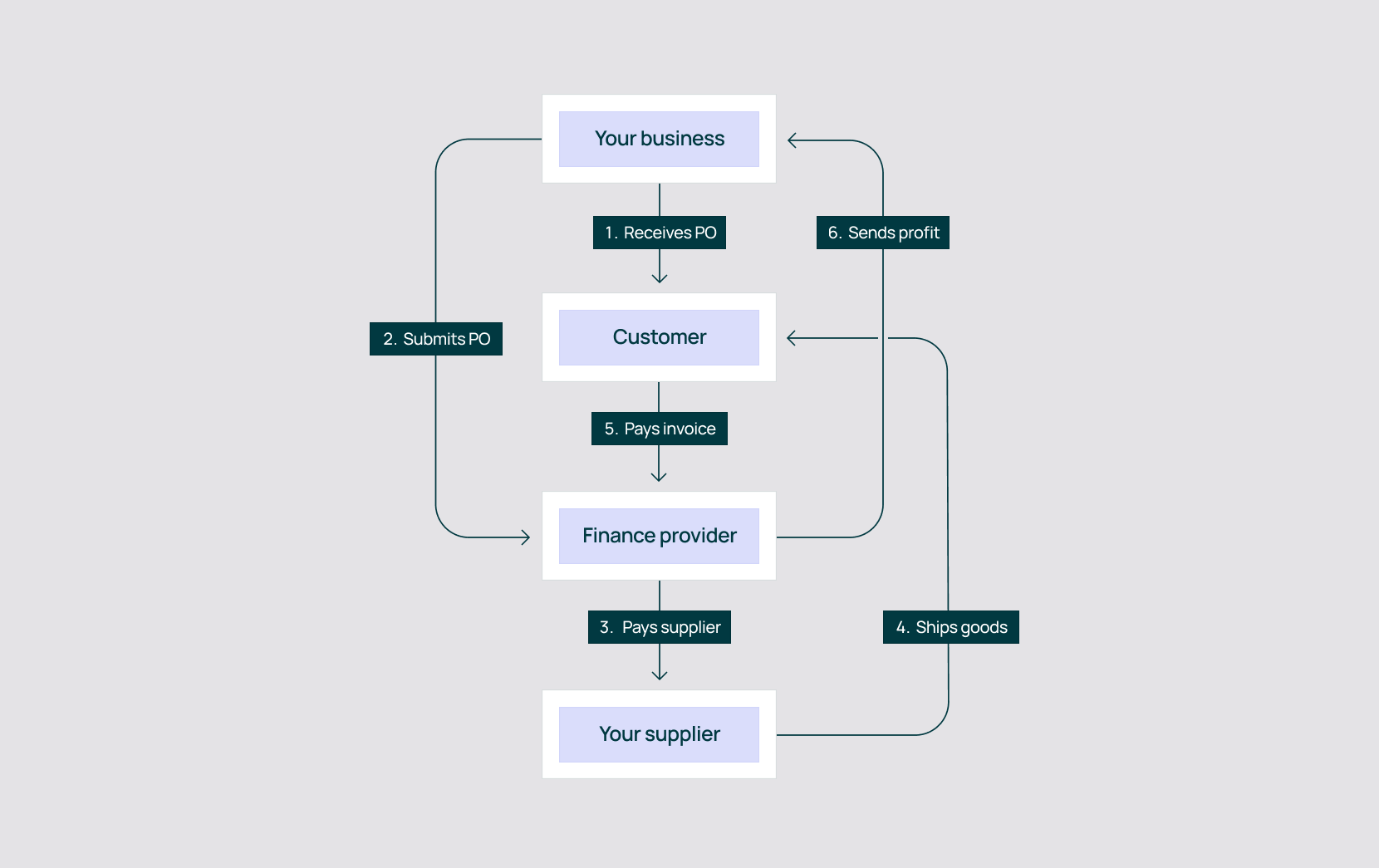

1. You receive a purchase order

The process starts when your business receives a confirmed purchase order from a customer. This order outlines the products, quantities, and agreed payment terms, signalling future revenue. Before proceeding, ensure the purchase order is valid and confirmed to avoid issues later and meet customer expectations.

2. You submit the purchase order to a financing provider

Once confirmed, submit the purchase order to a financing provider. The provider evaluates the order, the customer’s creditworthiness, your supplier’s reliability, and your ability to fulfil the order.

Approval determines how much funding will be released to cover supplier costs. Modern fintech solutions, like Triffin Credit, streamline this step with online submission and quick approvals.

3. The provider pays your supplier

After approval, the provider pays the supplier directly, usually covering 80–100% of the costs. For international orders, Letters of Credit may be used to guarantee payment. This ensures suppliers can produce, package, and ship products without delay, removing the cash-flow gap and enabling timely order fulfilment.

4. You fulfil the order and deliver to the customer

With funding in place, your business manages logistics, shipping, and delivery. The customer receives their order on time, while the financial operations remain seamless in the background.

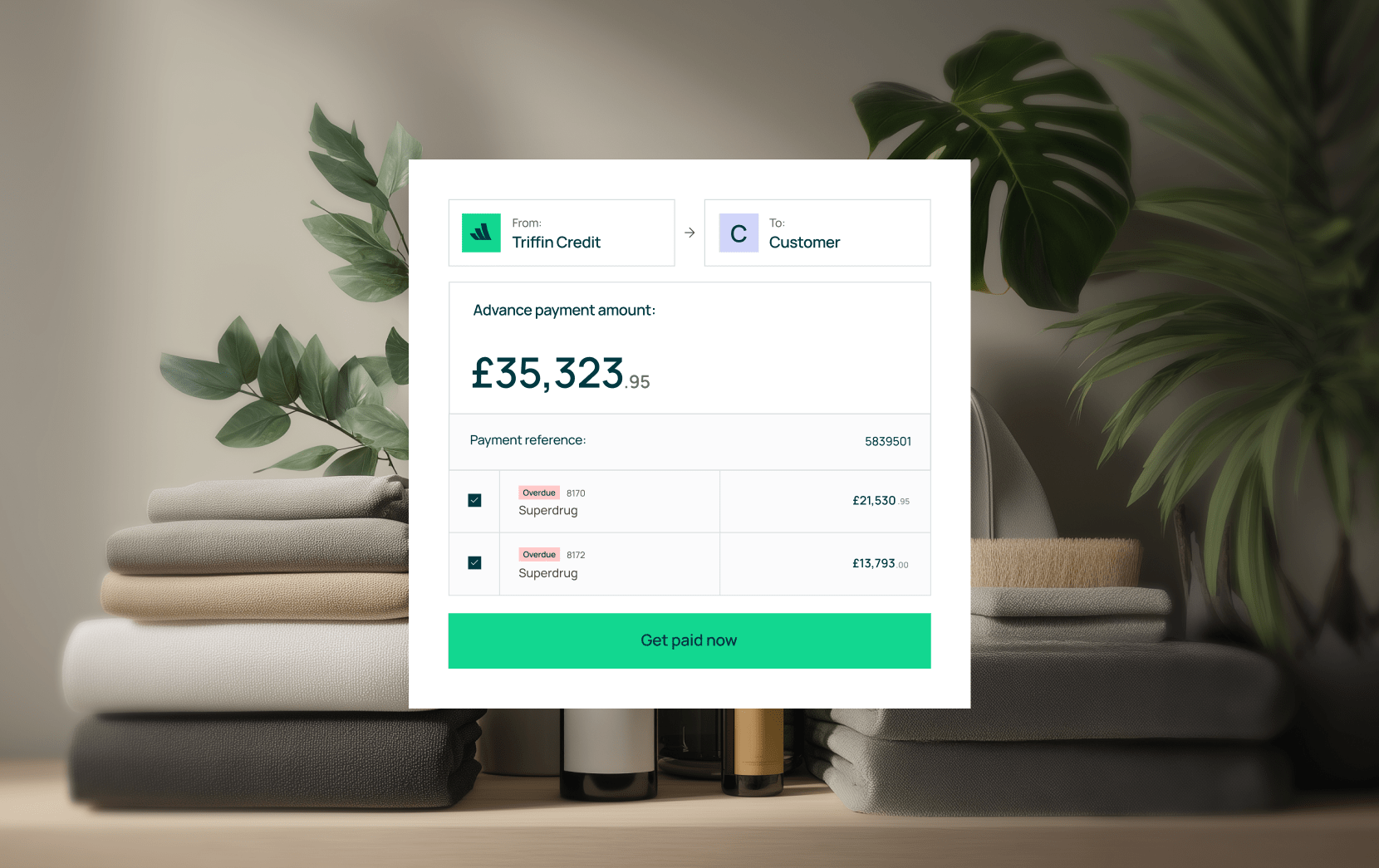

5. The customer pays the financier

Once the order is delivered, your business invoices the customer and sends a copy to the financier. The customer pays the financier directly, who deducts fees (typically 1–6% of supplier costs per 30 days) and sends the remaining profit to your business. This step functions like invoice factoring, converting receivables into immediate cash while transferring payment risk to the financier.

Improved cash flow

Purchase order financing helps businesses maintain healthy cash flow by providing the funds needed to pay suppliers upfront. Instead of waiting for customer payments, you can access the capital needed to fulfil large orders.

Quick access to capital

With purchase order financing, you can access funds quickly, usually within a few days. This fast access to working capital allows you to scale your business and take advantage of growth opportunities.

No additional debt

PO financing is not a traditional loan. It's a transaction-specific advance, so it typically does not appear as debt on your balance sheet, preserving your credit capacity for other needs.

Flexibility for growth

Purchase order financing gives you the flexibility to expand product offerings and meet the demands of a growing customer base without worrying about upfront inventory costs.

Reduced risk of delays

With purchase order financing, supplier costs are paid upfront, reducing the risk of delays in fulfiling customer orders. This helps ensure timely delivery, boosting customer satisfaction and loyalty.

Transaction-focused

Financing is secured against a specific, verified customer order rather than your business’s overall assets or credit history. This means you can access funding based on the strength of the order itself, making it easier for growing businesses to take on large orders without relying on extensive credit checks.

Strengthens supplier relationships

Guaranteed, timely payments from the financier ensure your suppliers are paid on schedule, which can help you negotiate better terms, secure priority production, and build long-term trust with key partners.

Costs and fees

Purchase order financing comes with fees, usually a percentage of the order value. While immediate access to funds is beneficial, these costs can reduce profit margins, particularly for businesses that rely on financing frequently.

Dependence on customer payments

The financier relies on your customer paying on time. Delays in payment can create cash flow issues, as the financing provider must still be repaid. This dependence introduces a risk to your financial stability.

Limited control over collections

In PO financing, which often integrates invoice factoring, the provider may handle the collection process. This can reduce your control over customer interactions and, if handled poorly, may affect relationships or your brand reputation.

Eligibility restrictions

Not all orders or customers qualify. Providers assess your customer’s creditworthiness and the order value before approving funding. If the criteria aren’t met, you may be unable to secure financing, limiting opportunities.

Impact on margins

Fees can accumulate, especially when financing multiple orders. While PO financing offers cash flow relief, the long-term cost may affect overall profitability if not managed carefully.

Operational over-leverage

Because it provides fast access to capital, businesses may be tempted to accept more orders than they can operationally handle. This can strain your management capacity and lead to delays or quality issues if not carefully managed.

Limited scope

PO financing typically only covers direct supplier costs for the specific order. It generally does not pay for overhead, payroll, marketing, or other inventory needs, which can still strain your cash flow.

Learn more about how Triffin can help your business

Triffin streamlines PO financing through a single, integrated platform. You get quick online approvals, and our AI agents handle documentation and administrative tasks, saving time and reducing complexity compared with managing separate lenders or manual processes.

Yes. Triffin Credit is a revolving facility, not just a one-off loan. Once approved, you can draw funds for multiple inventory purchases or get instant payment on invoices without reapplying each time, supporting ongoing growth.

Our AI finance agents protect margins and smooth operations. The Collections Agent helps secure faster customer payments, while the Financial Analyst Agent gives clear insights into the cost and profit impact of each financed order, helping you make smarter business decisions.

No. You remain the primary point of contact with your customers throughout the process. While the financier typically collects payment directly after fulfilment, Triffin ensures this happens smoothly and professionally without interfering with your commercial relationships.

Triffin offers quick online approvals, allowing you to move fast when new orders come in. Once your credit facility is active, decisions on draw requests are usually made within 4 hours, and supplier payments follow in line with the financing partner’s disbursement process.

“Triffin gives me the insights and financial confidence - every single day down to a granular level, I can see my financials - It's my number one”

“Triffin is a game-changer for cash flow! I love how the sales & marketing agent splits our performance by market”

“With Triffin we can launch new markets and new product lines in a low-risk way, it’s been a fundamental change in how we run the business leading to triple-digit growth.”

“The financial analyst agent keeps our business on track. It’s ability to surface COGS/Postage/Pick & Pack on a per order level makes analysing our margins at a granular level so easy, without needing spreadsheets.”

“Getting agent reminders on what to pay and when removes a lot of the hard, manual admin work, it makes our weekly pay-runs easy. I love the analyst agent's 3D avatars!”