Turn unpaid B2B invoices into immediate working capital. Triffin Credit helps UK & Irish retail and ecommerce brands access funds quickly, reduce cash-flow pressure, and keep inventory moving. Say goodbye to slow payments and ensure your business can grow confidently, without waiting weeks for B2B customers to settle their B2B invoices.

• Boost Cash Flow Quickly

• Fund Growth Without Adding Debt

• Save Time on Financial Tasks

Triffin makes managing cash flow simple and stress-free for growing brands. With fast access to working capital, intelligent AI finance tools, and flexible credit options, we help businesses unlock growth, optimise margins, and focus on what they do best. Unlike traditional lenders, Triffin combines technology and financial expertise to give you control, clarity, and confidence in every financial decision.

Get paid instantly on outstanding B2B invoices without waiting

AI agents automate cash flow tracking and payment processes

Revolving credit supports inventory, growth, and operational needs

Invoice financing lets you unlock cash from unpaid B2B invoices instead of waiting weeks or months for B2B customers to pay. So rather than carrying the burden of long payment terms, you receive most of the invoice value upfront, then repay once the customer settles the bill.

It’s a simple way for brands to turn completed orders into immediate working capital. You keep cash flowing, restock inventory faster, and avoid the pressure that comes from delayed payments.

For product businesses juggling suppliers, production cycles, and rising demand, invoice financing acts like a release valve, giving you liquidity exactly when you need it.

Invoice financing sits under two main structures:

A. Invoice factoring

Invoice factoring means you sell your B2B invoices to a finance provider (the factor), who advances most of the invoice value upfront and then collects payment directly from your B2B customers. This is visible to the customer because the factor takes over credit control.

Examples:

• A supplements brand sells £40,000 of wholesale invoices to a factor and gets an advance of £34,000 within 24 hours.

• A cosmetics company facing long retail payment terms uses spot factoring to fund a single £15,000 invoice from Boots.

Key variations:

• Recourse vs non-recourse: Determines whether you or the lender absorb the loss if the customer doesn’t pay.

• Whole ledger vs single invoice: Finance all B2B invoices or only selected ones.

B. Invoice discounting (often called Invoice Financing)

Invoice discounting uses B2B invoices as collateral for a confidential cash advance. You retain control of customer relationships and continue collecting payments yourself.

Examples:

• A skincare brand draws £50,000 against outstanding wholesale invoices from Boots instead of waiting 90 days for payment.

• A food and drink brand uses selective invoice discounting to finance two B2B invoices from major retailers while keeping the rest in-house.

Key variations:

Selective invoice discounting: Finance only the B2B invoices you choose, giving you flexibility to unlock cash selectively without committing your full ledger.

Whole ledger discounting: Finance your entire sales ledger, providing consistent access to working capital across all B2B invoices.

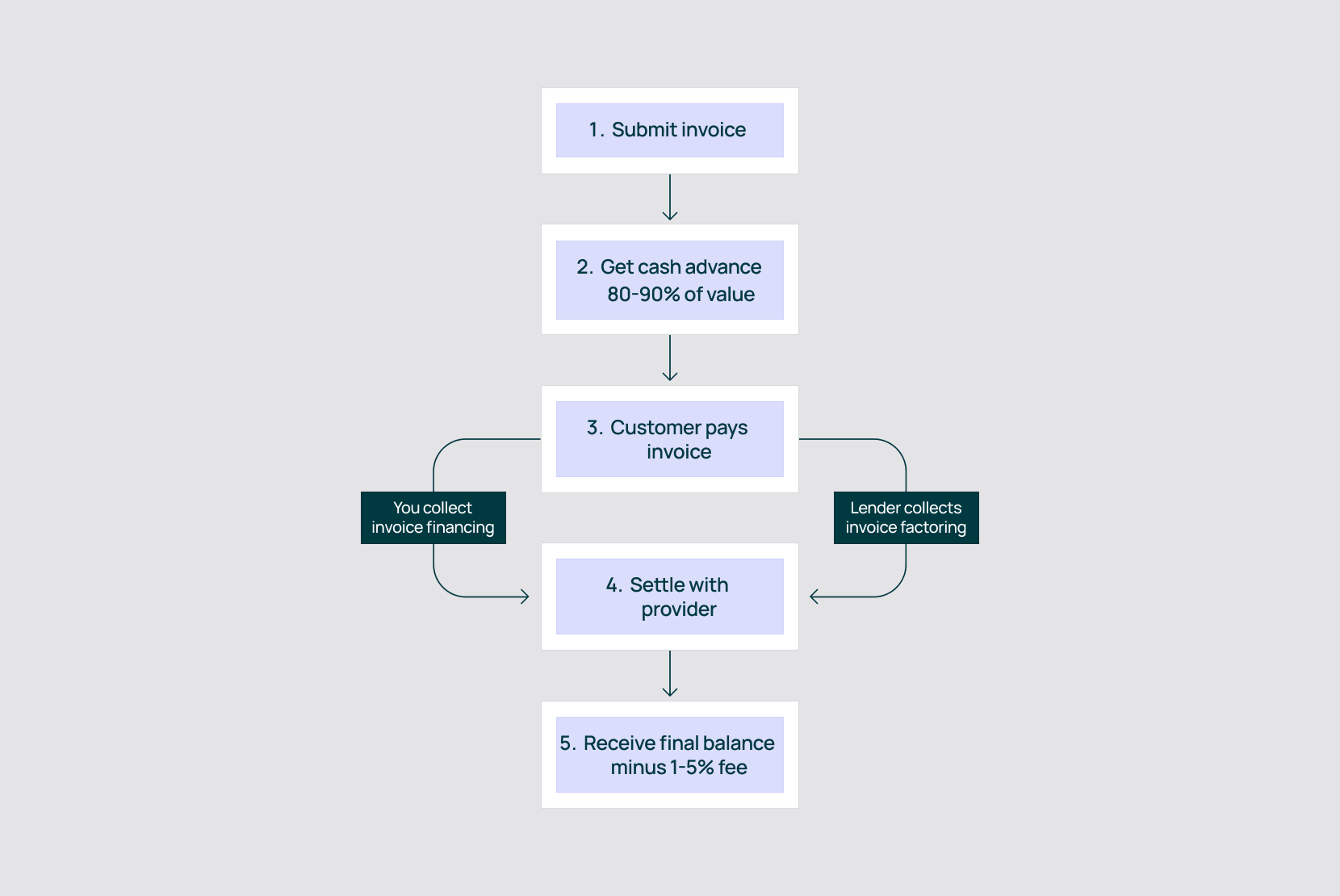

1. Invoice submission

Start by submitting your unpaid B2B invoices to the financing provider. They review key details: customer name, amount owed, and due date, to confirm the invoice is valid. Once verified, the lender assesses the customer's reliability and decides whether the invoice qualifies for funding.

2. Funding approval

Approval is based mainly on your customer’s creditworthiness, not your own. The provider checks the buyer’s payment history and ability to settle the invoice. If everything checks out, the lender approves the invoice and confirms the amount they can advance.

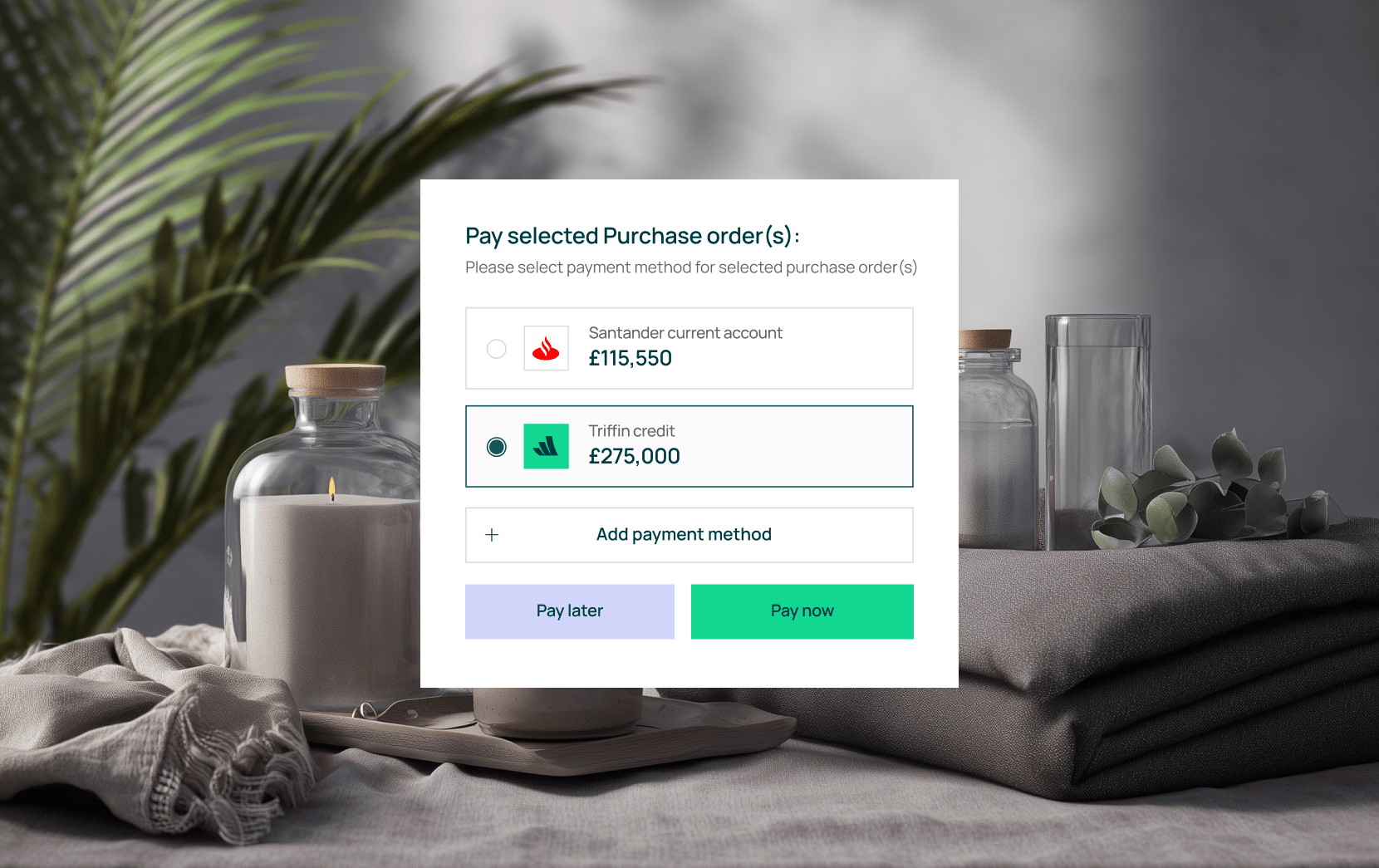

👉Triffin bases approval decisions on your brand's creditworthiness, not your B2B customers'.

3. Advance payment

After approval, most providers will offer you an advance of 80–90% of the invoice value. This gives you immediate working capital for inventory, marketing, payroll, or other operational needs, without waiting weeks for payment.

👉Triffin lets you access up to 100% of your invoice value upfront.

4. Customer payment

How payment is collected depends on the structure:

• Invoice Financing (Invoice Discounting): You continue collecting payment from the customer, usually confidentially.

• Invoice Factoring: The lender collects directly from your customer.

Once the customer pays, the provider receives or confirms the funds.

5. Final payment and fees

The lender releases the remaining balance to you, minus their fee (typically 1–5%). This fee covers the cost of advancing funds and managing the facility. With the balance paid out, the transaction is complete and the cash cycle resets for your next invoice.

👉Triffin offers flexible repayment: choose monthly payments or a bullet repayment, with terms from 2–6 months.

Improves cash flow stability

Invoice financing helps you access money tied up in unpaid B2B invoices, giving your business steady cash flow even when B2B customers take weeks or months to pay. This stability allows you to plan ahead confidently, cover expenses on time, and avoid interruptions in production or daily operations.

Supports day-to-day operations

With quicker access to funds, you can stay on top of essential expenses like payroll, inventory, rent, and supplier payments. Instead of waiting for delayed B2B invoices, you keep your operations running smoothly and maintain a professional reputation with staff and partners who rely on consistent, timely payments.B2B buyers commonly impose payment terms of 30, 60, or even 90 days. You manufacture products, ship to distributors or buyers, and wait months for payment while still needing to fund the next production cycle. Wholesale financing advances cash immediately, letting you maintain operational momentum without the constant pressure of delayed revenue.

Enables faster growth and expansion

When your cash isn’t tied up in unpaid B2B invoices, you can invest in the things that help your business grow sooner. This might mean

• Restocking inventory

• Taking on more orders

• Boosting marketing, or

• Improving your operations.

Provides flexibility

Unlocks money you’ve already earned without adding long-term debt or fixed monthly repayments. While it is still a form of borrowing with associated costs, the key advantage is that funding scales with your sales; the more B2B invoices you issue, the more working capital becomes available.

Reduces financial stress

Waiting 30–90 days for B2B customers to pay can create uncertainty and pressure. Invoice financing reduces that stress by giving you predictable access to cash when you need it. It helps you stay calm, focused, and prepared, with little to no worry about how long payments will take or whether you can keep everything running.

Strengthens customer relationships

It allows you to offer clients extended payment terms (like net-60 or net-90) as a competitive advantage, while you still receive immediate cash flow, satisfying both parties.

Improves accessibility vs. traditional loans

Approval relies more on your B2B customers' strong creditworthiness than your business's credit history or collateral, making it easier for newer or smaller businesses to access capital. With Triffin Credit, we base approval on your brand's performance rather than your B2B customers' payment reliability, giving you even greater flexibility.

Costs and fees

Fees typically fall within the 1–5% range per 30 days, but they are often prorated weekly or daily. This means your total cost depends heavily on how quickly B2B customers pay. Slow-paying clients increase your financing cost, and many providers add extra charges such as service fees, monthly minimums, or early-termination fees.Wholesale financing costs money. Interest rates, fees, and facility charges vary by provider and financing type. Even relatively affordable wholesale financing typically costs more than traditional bank loans but remains cheaper than equity dilution. You need to ensure the margin improvement from bulk ordering or revenue from additional orders exceeds the financing cost.

Reliance on customer creditworthiness

Eligibility and pricing depend largely on your B2B customers’ credit strength, not your own. If your B2B customers have inconsistent payment histories or are seen as high-risk, lenders may restrict your funding limit or raise fees.

With Triffin Credit, approval is based on your brand's creditworthiness, so this limitation doesn't apply.

Limited control over collections (factoring Only)

With invoice factoring, the financier manages payment collection directly with your B2B customers. This reduces your control over communication and can introduce a tone or process you wouldn’t choose yourself. This drawback does not apply to invoice discounting, where you retain full control.

Short-term solution

Invoice financing is best used as a tactical cash-flow tool, not a long-term fix. Experts advise implementing strong internal Accounts Receivable processes first; relying on financing as a crutch can mask structural cash-flow issues.

Potential impact on customer relationships (factoring only)

Because the factor contacts your B2B customers for payment, there is a risk of friction, especially if their collections approach feels aggressive or unfamiliar. Discounting avoids this issue because it remains confidential, and customer interactions stay with you.

Risk of customer default

Most factoring agreements are with recourse. This means if your customer fails to pay the invoice, you are liable to repay the advance and fees to the lender, not the financing company. You can get "non-recourse" protection, but it is more expensive and usually only covers customer insolvency, not payment disputes.

Potential for administrative complexity

Mismatched invoice tracking or reconciliation errors between your books and the lenders can create administrative friction and even harm customer relationships. Ensuring you or your lender uses accurate, automated systems is important.

Learn more about how Triffin can help your business

Most Triffin Credit applications are approved within 48 hours, giving you fast access to working capital once your B2B invoices are verified.

With Triffin Credit, you can typically access 100% of your invoice value upfront. This gives you predictable cash flow while reducing the wait for payments.

No. With invoice financing via Triffin, you continue collecting payments yourself confidentially. This ensures your customer interactions remain professional and consistent.

Yes. Triffin Credit is designed for UK and Irish retail and ecommerce brands with £1M–£20M in annual revenue.

No. Triffin Credit operates with full transparency. There is a simple, fixed monthly facility fee to keep your credit line available, with no hidden charges or complex long-term contracts.

Triffin Credit gives you flexibility in how and when you repay. Choose between monthly payments or a bullet repayment (paying principal plus fees in one lump sum at the end of the term). You can also select a repayment timeframe between 2–6 months to suit your cash flow cycle.

“Triffin gives me the insights and financial confidence - every single day down to a granular level, I can see my financials - It's my number one”

“Triffin is a game-changer for cash flow! I love how the sales & marketing agent splits our performance by market”

“With Triffin we can launch new markets and new product lines in a low-risk way, it’s been a fundamental change in how we run the business leading to triple-digit growth.”

“The financial analyst agent keeps our business on track. It’s ability to surface COGS/Postage/Pick & Pack on a per order level makes analysing our margins at a granular level so easy, without needing spreadsheets.”

“Getting agent reminders on what to pay and when removes a lot of the hard, manual admin work, it makes our weekly pay-runs easy. I love the analyst agent's 3D avatars!”